How Much Is Your Working Capital Really Costing You?

By: By John Tsai, PhD, Head of Analytics, and Charlotte Ng, Chief Product Officer

Published June 24, 2026 | Estimated read time: 2 min

For small and medium-sized businesses (SMBs), access to working capital is often the difference between growth and stagnation. Yet many business owners evaluate financing options primarily by comparing interest rates. While interest rates are important, they can obscure the true economic cost of financing.

In this post, we lay out why businesses should consider the total cost of financing when evaluating working capital products, and how OneAM Early Pay gives businesses the control and flexibility to align their financing with working capital needs.

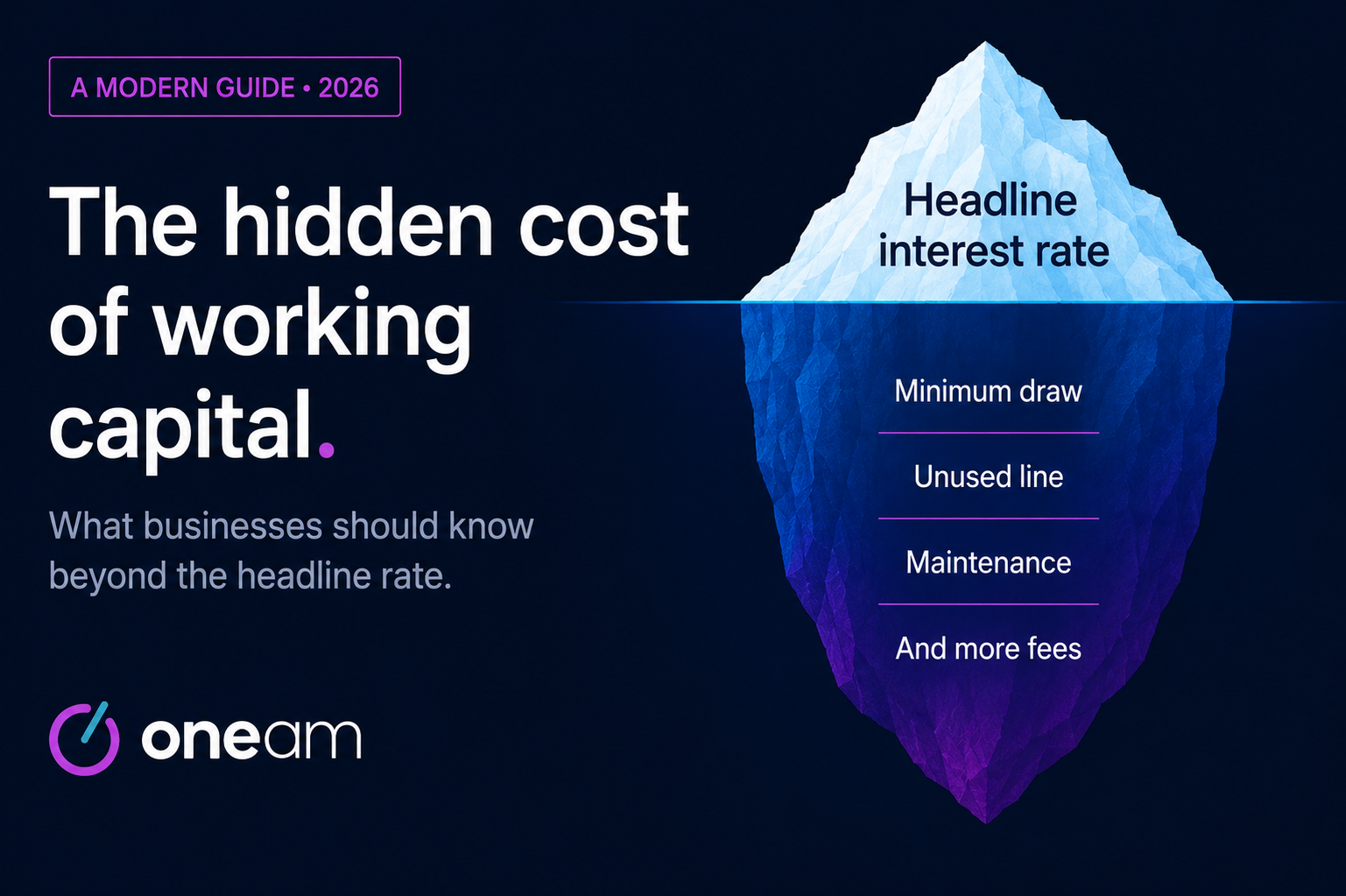

Evaluating the True Cost of Financing

To understand the actual cost of obtaining sufficient working capital, companies should consider the total dollars spent on financing, in addition to interest rates. The reason is simple: the total dollar amount of interest and fees paid over the course of a year represents the real financing cost. A lower rate does not necessarily translate into a lower financing expense if a business is forced to borrow more capital than it actually needs, or to maintain outstanding balances regardless of its operating requirements.

This is precisely the challenge faced by SMBs. Aside from bank lines of credit—which are the lowest-cost option for accessing working capital, provided a business qualifies and the owner is willing to take on the huge risk of a personal guarantee—most commercial facilities are rigidly structured. Products such as asset-based loans (ABLs) or minimum-volume factoring contracts often require borrowers to maintain a minimum drawn balance or keep a portion of the facility outstanding at all times.

In addition, these facilities may include commitment fees, utilization fees, maintenance fees, and other charges that increase the effective cost of borrowing. At the most expensive end of the spectrum, with merchant cash advances and revenue-based financing, borrowers receive a lump sum upfront and pay a massive premium for cash that might sit undeployed.

Unpacking the Math Behind the “Low” Rate

Consider why a business might take out a large facility in the first place. Working capital needs fluctuate due to seasonality or growth, so to be conservative, businesses often size their loans to cover their peak needs, not average needs. Furthermore, commercial lenders tend to enforce minimum facility sizes to cover their own operational and underwriting costs.

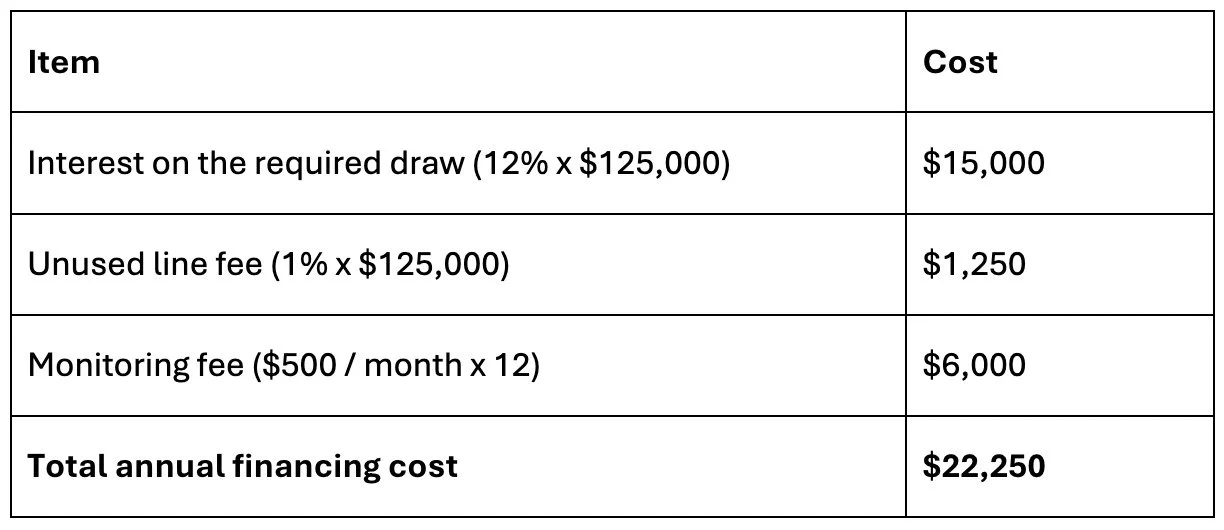

To see how this plays out, consider an SMB that takes out a $250,000 commercial facility to cover their seasonal peak, but on average only needs $75,000 throughout the year. The lender has a headline interest rate of 12%, requires 50% minimum draw ($125,000), charges a 1% unused line fee, and adds $500 a month in monitoring fees.

The SMB pays over the course of a year:

Even though the facility may have a 12% headline rate, the effective APR, or true economic cost, is closer to ~30% ($22,250/$75,000 average capital need).

From an economic perspective, this is an unnecessary expense. Borrowing cash that sits idle on a balance sheet does not fund growth, purchase inventory, or create value for the business. Yet, under many commercial financing structures, companies feel they have little choice but to absorb these sunk costs just to maintain a financial safety net.

OneAM Early Pay: Flexible Working Capital for When You Need It

OneAM Early Pay enables businesses to convert their accounts receivable into cash, allowing them to access capital when they need it and avoid drawing capital when they do not. Because businesses are charged only for the capital that is actually used, funding size, duration, and costs match real working capital needs.

Unlike many rigid commercial working capital options, OneAM Early Pay puts control back in the hands of the business:

No hidden fees: We charge no origination, platform, or maintenance fees.

High flexibility: There are no minimum volume requirements or lock-in contracts; you choose which invoices to fund.

Transparency upfront: We provide complete transparency into your total financing costs.

We understand that businesses often experience fluctuating working capital needs driven by seasonality, inventory cycles, customer payment timing, project-based revenue, or growth initiatives. By matching capital availability to actual business requirements, OneAM Early Pay eliminates much of the waste found in commercial financing structures.

The result is a much more efficient approach to working capital management—one that can significantly reduce total financing costs while providing businesses with access to capital when they need it.