Is Your Business Ready for What’s Next? Bracing for Turbulence

By: Charlotte Ng, Co-Founder & Chief Product Officer, OneAM

Published Tuesday, April 15, 2025 | Estimated read time: 3 min

Of the myriad decisions that business owners have to make every day, some of the most important and toughest ones have to do with financing. In a survey by Goldman Sachs, 53% of small businesses could not afford to take out a loan at current interest rates; 35% have applied for a new business loan or line of credit and 80% of them reported it was difficult to access affordable capital. As the current macro volatility continues, we’ll look at the turbulence we’re seeing in business financing and why shoring up liquidity with non-debt solutions makes sense.

Uncertainties at the SBA

In recent weeks, the Trump administration announced a 43% cut to the Small Business Administration (SBA) workforce as well as the transfer of the Education Department’s $1.6 trillion student loan operation to the SBA. The SBA provides loans which are guaranteed by the government. This makes the loans less risky for banks, enabling them to pass lower interest rates on to the borrowers. According to the Department of Treasury, the U.S. small business loan market is valued at $1.4 trillion and new SBA 7(a) loan issuance totaled $31 billion in 2024. With these disruptions, we expect the agency to turn its focus on the drastic internal overhauls, and some applicants for SBA loans could face longer loan processing times.

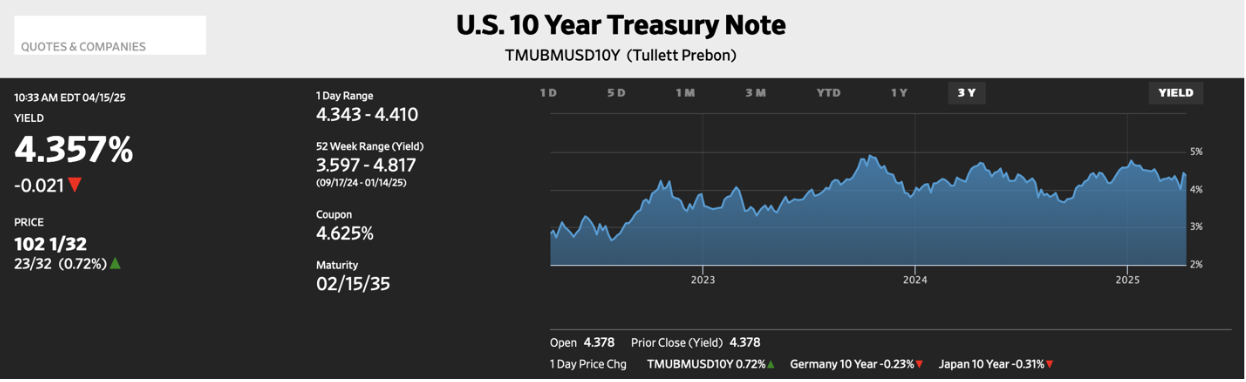

Interest rates stay elevated

Capital markets geeks like us have been anxiously watching U.S. treasury yield movements. Following the tariff news last week, we witnessed a joint selloff of both stock and bond markets, an unusual occurrence. U.S. treasury yields are foundational to the cost of borrowing, and higher yields mean higher borrowing costs.

Even with the pause on some tariffs, major tariffs on China, Mexico, and Canada remain in place, and these trading partners contribute the bulk of U.S. imports. The inflationary pressure from tariffs limits the ability of the Federal Reserve to preemptively cut rates even with a softening economic outlook.

What this means for business owners is that taking out loans and refinancing will stay expensive and there’s little imminent relief.

Source: Wall Street Journal

How non-debt solutions like OneAM can help

In a turbulent macro environment, shoring up cash is a sensible risk mitigation strategy for any business. With OneAM, your receivables can be quickly turned into another source of cash, complementary to your business loans and credit cards. As a non-debt solution, receivables financing doesn’t add a liability to your balance sheet. Our highly flexible structure gives you control of your liquidity and allows you to protect against delayed customer payments.

OneAM connects businesses selling receivables with sophisticated institutional investors, offering a faster, more business-friendly alternative to traditional factoring. In an environment where making long term predictions is harder than ever, the ease and speed of our financing platform allows business owners to add an additional layer of protection whenever they need it.

Learn more on our website or schedule a demo at info@oneam.us.